How to grow your crypto investment completely tax free (US residents)

In this post, I would like to explain the structure that I am using that you can implement in order for your crypto investment to grow completely tax free.

Short term and long term gain tax

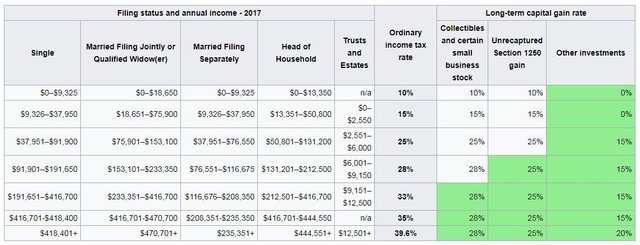

Crypto investment has high potentials and this has become one of the great interests of IRS. IRS treats crypto as property for tax purposes. That means if you buy bitcoin with USD and then use bitcoin to buy other alts that would be a tax event. Many people think that the tax event is only triggered when they cash out to USD but no. Any time you make an exchange this is considered a tax event. If you hold a crypto-currency for less than a year and trade it for another crypto-currency or fiat currency, you are taxed at your income tax rate which varies between 10 to 40% depending on your tax bracket and income range. However if you hold it more than a year then you are taxed as long term gain which is lower. Notwithstanding, you have to pay the tax! In the best case scenario let's say you invested $100k in crypto and after 2 years it grow to $1M. Then you have to pay 15% tax on your gain meaning $135k.

Is there a legal way to avoid taxes for our investments?

The answer to this question is YES! Believe it or not, you can put up a legal structure for your investment to avoid both short term and long term taxes. In a nutshell you only need to use a ROTH self-directed IRA as an investment vehicle.

What is a "Self directed IRA" and why it is important to structure it as Roth IRA rather Traditional IRA?

IRA stands for Individual Retirement Account. There are many types of IRAs that you might have heard of. 401(k) is one type of IRA that you can contribute through your employer and the custodian give you options of bonds and stocks to chose. Any IRA can be in two type: 1- traditional IRA and 2 - Roth IRA. Here is the difference:

- Traditional IRA: You contribute your pre-tax money to this account. The investment grows over years and you get retired. Once you are 60 years old you can withdraw money from this account but you will have to pay tax on the withdrawal amount because you did not pay tax when you contributed. For example if you contribute $10k of your pre-tax money and it grow to $100k over years, and you want to withdraw $20k from it after you are retired you have to pay tax on the whole $20k amount and also on any subsequent withdrawal from that money.

- Roth IRA: This is an IRA where you can contribute your post-tax money. And when your investment grows, you do not need to pay any tax what so ever on the gain when you retire and want to withdraw the money. This is HUGE positive of the Roth structure that many people are not awar of. Lets say you contribute $10k to Roth IRA (you have to pay tax on it first so it becomes post-tax) and your investment grows to $100k over years. Whenever you want to make any withdrawal after you are 59 years old there is absolutely NO tax whether short-term or long term. No Tax! If you want to withdraw that money before you are 59 years old you should pay 10% penalty on the gain (and not on your initial investment) which is much less than the income tax and capital gain tax rates.

As I mentioned above there are different IRAs. like 401(k) where you contribute through your employer. There is another type called "Self Directed IRA" which is a vehicle for individuals who want to invest their own money into anything they like. There are some restrictions however with regards to this investment and IRS call it "prohibited transactions". And that basically mean any transaction that benefits you and your family. This is because your IRA should be treated as a separate legal entity than you because it is not you it is future you! So let's say if you open a self-directed IRA and buy a home with it, you or your family cannot benefit from that home. You cannot live there or you cannot rent it to your son! This will be a prohibited transaction and if IRS finds out your whole asset is subject to immediate liquidation with severe penalty and you will lose the majority of your wealth. However, you are able to rent that home to a third party and collect the rent for your IRA. The rent money will go to your IRA account for the benefit of your IRA (and not for your benefit).

With regards to crypto investments, the most optimum structure is you invest through your self-directed Roth IRA.

How can I invest in crypto through a self-directed Roth IRA?

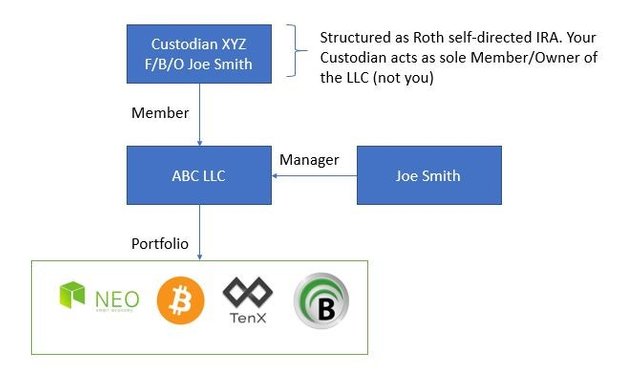

Whenever you set up a self-directed IRA (whether Roth or Traditional) you have to set it up with a custodian. There are plenty of custodians out there that will do this for you. However, everytime you want to invest in something it needs to go through the custodian. For example, you find a good real estate opportunity and would like to invest. You can't just go and write a check from your IRA account and buy that home, you have to first contact your custodian and advise them to wire the money to the seller and then the home will be in the name of your IRA. The title of the home will be look like this: Custodian XYZ F/B/O Joe Smith (you).

There are some custodians in US that allow you to invest in crypto. But the downside with them is the options of the investment is so small only bitcoins and a few more altcoins and everytime you want to make a trade you have to go through them. That is not really practical. However you can circumvent this by establishing a LLC (a new company) and have your custodian to invest in that LLC. In this way you only need permission once and for all from your custodian. Once the money is wired to that LLC checking account, you can literally invest in anything you want on any exchange you want! The important thing here is that you will act as the Manager of that LLC and not the member/owner of the LLC. The owner of the LLC is your IRA. and your IRA (aka the investor) appoints you as the manager of this company so you will have full authorization to make any decision for the company. The best part of structuring a LLC is that LLC does not pay any tax (vs a c-corporation has to pay tax on its own level). In LLC, the tax would follow through to the owner of the LLC. In this case because the owner of that LLC is a Roth Self-directed IRA there is no tax liability what so ever.

Once you put this structure in place, lets say you invest $100k and this grow to $1M in a few years. When you want to withdraw this money from your IRA you absolutely pay NO tax at all. event once cent. Because you put this as Roth IRA. If you are less than 59 years old and want to withdraw that money you only pay 10% penalty for early withdrawal (and still no tax at all) which is much better that regular tax rates (short term and long term). There are also some exceptions that you can avoid this 10% penalty! for example if you are the first home buyer and buy a home for $500k you don't need to pay anty penalty. Or another example if you want to pay for your children's college tuition you are exempt from paying that penalty. Many people can't believe that this is true! But this is actually true! and there are so many loopholes in the tax regulations that wealthy people are taking advantage of and avoid paying taxes in this country. Why do you think wealthy people pay the least amount of tax here in US because the know the loopholes and they are taking advantage of it!

Step by Step Instructions

- Find a custodian who is okay to invest in an LLC with you being able to invest in crypto

- Transfer your post-tax money to the custodian and structure a Roth self directed IRA

- Incorporate a LLC in your state (make sure in your state the LLC does not pay tax). You will need a lawyer to draft the LLC Operating Agreement for you. Your custodian will sign the Operating Agreement and appoint you as the manager of the LLC.

- Once the LLC is incorporated take the documents to a bank and open a business checking account for your LLC

- Advise your custodian to write a check in the name of your LLC

- Deposit the check in to your business checking account of your LLC

- Open an institutional account with itBit.com

- Wire money from your LLC checking account to itBit.com and buy Bitcoin with it

- Open an institutional account on Bittrex.com with a new email address in the name of your LLC

- transfer the bitcoin to your Bittrex account and buy any altcoin you desire (let's say NEO)

- Transfer your NEO to a new NEO wallet account (please make sure you never mix this money with your own money because this will trigger the prohibited transaction and you will lose all your money)

- Keep your NEOs for a couple years and enjoy!

- After a few years your NEO is worth $1000 and you want to cash out some money. Do the reverse, transfer your NEO to bittrex and then buy bitcoin, transfer bitcoin to itBit.com and have them wire the money to the LLC checking account

- Write a check from your LLC checking account to your IRA

- Advise your IRA to distribute the money to you. If you are less than 59 years old you will have to pay 10% penalty but again you can also avoid that fee in some situations.

So I spent significant amount of time and several thousands of dollars on legal fees to figure out this structure and set it up correctly. If you found this post useful and would like to make some donations please see below:

BTC: 1MWLWiNJs4pN33cddokn2UMDJ4NZiSLVGm

NEO: AYBzQ2HnDhsfr8ir6cu9zZ8dnRscMYj1VM

ETH: 0x526a1ae076424f4d874250526dab7bd1f70a44fd

Following this strategy wouldn't allow you to avoid reporting the gain on your tax return (in the case of an early distribution). You would pay not only the 10% additional tax, but you would also owe taxes on the gain that you would be forced to report. If you're treating the LLC as a subchapter C entity, the IRS would likely look through the transaction and subject you to the same tax implications as if the entity did not exist. See the example with Justin in Publication 590-B.

https://www.irs.gov/publications/p590b#en_US_2016_publink1000231064

I live in the Netherlands so it doesn't concern me,but Nice artikel

If you make approximately a million dollars, you will NOT be in a 15% bracket for because it is taxable at your marginal income tax rate, or 39.6%. If it is a long term capital gain, then your capital gains are capped at a tax rate of 25%,

Not to mention there are contribution limits on IRA's as well as income related contribution limits that are specific to Roth IRAs as well as a penalty tax for excess contributions that remain in the IRA accounts. I'm pretty sure the wealthy don't benefit from Roth IRA due to income limitation.

Edit: I believe 39.6% bracket = 20% cap gains.

What is making me cringe is the example of making $10k contributions to an IRA is in excess of the statutory annual limit for an account. Beware of 6% penalty people....

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

To get around this, it is better to set up a Solo 40o1k with checkbook control. You have much greater depository limits (above $50k+) while enjoying many of the same benefits. The only caveat is that you have to be self-employed in some way... you must file a Schedule C showing income. So do something you might enjoy like start an Uber business or something that will send you a 1099. You can deposit the amount you claim on Schedule C income.

Grow it with airdrops: https://crypto-airdrops.de

Really enjoyed this post and want to thank you for its thoroughness. I did have a question though and would appreciate your input/feedback.

You mention setting up an institutional account with itBit, buying Bitcoin, and then transferring to a Bittrex institutional account. Just curious - why couldn't I just go straight to Bittrex and skip the itBit part (if Bittrex would accept my IRA LLC)? I guess I don't understand why that "itBit step" is needed?

Thanks again for the post!

@lordsaroman Excellent Post! I have done the same thing some years back. Finally just this past April I began to set up a corporate account with my LLC at a Crypto exchange. MAKE SURE YOU DON'T MIX FUNDS WITH PERSONAL (as mentioned above). I went with Kraken since I already had personal accts at Bittrex and Polo . BTW: Kraken took 5 weeks to approve and has terrible customer service, but it has been working well since. (resteemed)

You should still mention that there are fees associated with starting this type of set up that could change the cost-benefit for someone depending on the amount of money they are investing. I know fees can range from 1k to 2k, with some annual fees which may not help someone who is investing 500-2k in cryptos.

Simply WOW. Great read.

https://steemit.com/money/@dobartim/how-did-i-earn-from-usd-40-79-btc-for-8-months

Great post although I do not live in the US, it is very informative. Followed you, upvoted and resteemed