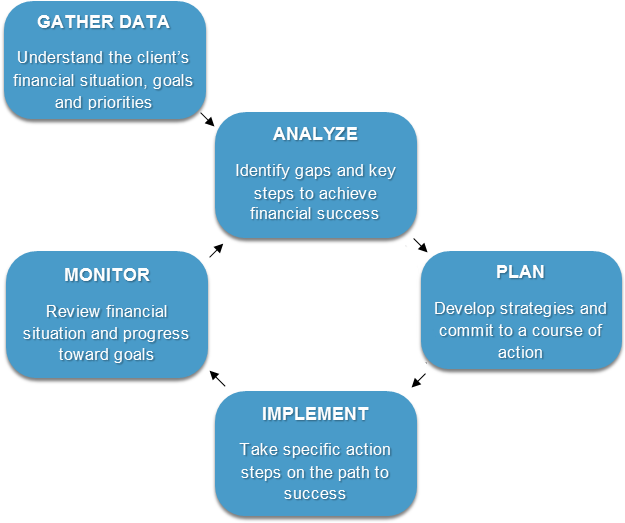

The paths to success in financial planning

Whether a CPA firm chooses to provide personal financial planning services or not, they will materially enhance the success of their clients’ financial future by looking to deepen relationships with their best clients.

It can be as simple as paying closer attention to the details and going just a little beyond telling them what happened last year.

A progressive and caring CPA should always take the opportunity to make sure that their clients are well-served across the financial spectrum. For years, many CPAs have told or alerted their clients about gaps in their personal financial lives — yet the same issues emerge year after year with the fix still not implemented. This has helped me to conclude that the incidental advice given to clients about related financial matters is a waste of time unless the CPA closes the gap by delivering the service themselves or making a specific introduction to the appropriate subject matter expert to close the gap.

Starting with those who chose not to provide wealth management services, pay close attention to the signals that a tax preparation engagement can send you. Some simple items such as noting that a client’s 1099s from bank or brokerage accounts are held in joint names are clear signals that there may not be an estate plan in place or that the plan in place is not complete or fully implemented. Most clients with significant assets should consider using trusts to hold title to their financial assets. If you notice the joint title and ask a question or two about their estate plan, you’ll quickly see whether they are in need of assistance.

Other financial matters that can be discovered through the tax prep process include items such as loss carry-forwards, excessive trading, or lack of trading in an investment account, retirement contributions and family governance. Loss carry-forwards, for example, may indicate a lack of coordination between the investment plan and the tax plan. This is something that may actually be the joint neglect of the investment advisor and the CPA, but don’t worry about who’s to blame. Suggest a solution or introduce a holistic wealth advisor who can coordinate these two moving parts of your clients’ financial lives.

Retirement contribution reviews can also originate a deeper discovery conversation. Asking if the client can afford to contribute more or if a different type of plan would be helpful is just the start. You can also ask where the money is invested and what the client’s process is for managing these assets. In many cases, you may be surprised to see that there isn’t much thought that goes into the investment choices being made inside the plan, and that an introduction to a qualified investment professional may be helpful.

Family governance matters can be discovered easily through the traditional accounting engagement. The joint ownership of rental property, for example, often reveals that there isn’t a partnership agreement or any other document that lays out the rules of engagement for that jointly owned property. Issues such as capital contributions, distributions from the property, and provisions for death or disability are frequently ignored when you discover rental properties held jointly.

Of course, there is no problem until there is a problem. But a problem such as your joint owner losing a lawsuit and getting a large judgment placed in their assets may put a crimp in your plans for that jointly owned rental property. These easily discoverable issues may impact your clients’ asset allocation, estate plan, tax plan and risk management plan.

These are clearly issues for a forward-thinking advisor. Again, even if you choose not to provide PFP services, this is a chance for you to help your clients with an introduction to a holistic financial professional with the ethics and intellectual capacity to oversee your clients’ entire financial lives.

Choosing not to provide the PFP service seems to be what many CPA firms are doing today. But sitting back and letting all of your clients’ open issues go by your tax prep or accounting services unnoticed, year in and year out, is not providing the best service that your best clients want, need and deserve from you.

For those firms that have decided to engage with PFP services, your first key to success lies in the awareness of these services by your clients and the willingness of your partners and staff to provoke client discussions. This may require highlighting some of the deficiencies or gaps that your accounting services have discovered in order for them to understand how you can help.

Many firms still keep their PFP service a secret. They keep it secret from their clients and they keep it secret from other financial services providers. Not telling those financial services providers that you’ve worked with before about your licenses and PFP divisions can be both disingenuous and deceitful. I’ve heard many reasons why CPAs choose to not be truthful with these other financial services providers. Many offer the fear that traditional referrals will stop. Not only is telling them the stand-up thing to do, but it may reveal opportunities to collaborate that may enhance both client service and your PFP division to everyone’s benefit.

Many would agree that CPAs might not be the best marketing and sales professionals in the financial world, but keeping the PFP division secret from your clients and staff is wrong. Your PFP efforts will never be successful if your clients are not aware of the offering. I’m not talking about cave man marketing where you obnoxiously try to push the service on every client; I’m talking about a tasteful marketing and communications plan that will have your clients keenly aware of these capabilities within a year or so. Over that time period, you want to build your clients’ confidence in your abilities to serve in the PFP space and encourage them to look at you differently. This is easily done, but will take time and effort. Many will quietly check you out, read your information, and visit your Web site to corroborate what you’ve been saying.

The next key is making sure that you’ve devoted the proper resources to market, communicate, and then deliver the services that you’ve marketed and communicated. Canned or white-label ghost-written marketing is better than nothing, but often not the best way to reach your clients. A customized approach that recognizes your firm’s current culture and client base will work best. This may focus on the niche markets that you serve or simply be written in such a way that it is consistent with the messages that your clients currently receive from you. The key is making the time to do this or finding the PFP partner who can deliver these critical marketing and communication services for your firm.

To succeed, the PFP division needs a leader. This leader must be responsible for everything from the marketing and communications, to building the service model, to proficiently and profitably offering the PFP services. For a firm with partners, collaborate regarding the business plan and set reasonable expectations. Expectations must be set for everything from revenue targets to the other partners’ roles in cross-selling these upscale and valuable services. For sole practitioners, it boils down to your willingness to create the necessary hours to drive this part of the practice. To succeed, your first year may take up at least 400 hours of infrastructure building and meetings from what used to be billable time. There is no short cut to success, and to some this barrier is simply too difficult to overcome.

Once you get the message out, the next key is to make sure that you are matching the service to the needs of the right clients. Many CPAs feel that they need to start with their smaller clients, where the stakes may be lower. This may work, but can become problematic as smaller engagements may take nearly as long as larger ones without the appropriate level of compensation for the firm.

Smaller clients may not need the full proactive and holistic wealth management process. Come up with a reduced service offering or simply pass on performing wealth management for clients who do not need the full proactive and holistic service. Your relationships with larger clients are often stronger than they are with your smaller clients. For this reason, the smaller client may be less forgiving about fees and billing and have unrealistic expectations that your service can make them wealthy. Your better clients often wish they could see more of you anyway, and the delivery of PFP services provides you the opportunity to do just that. Serve them at a higher level and spend more time with them. This will deepen your relationship and drive greater value in the overall relationship.

The key of keys

The last key, which is hidden in the previous paragraph, is that the most success is being garnered by offering a proactive and holistic wealth management process. Too many CPAs focus on investments or insurance, and end up offering a service that is no better than any previous service providers that your clients may have engaged. Don’t be like the others and merely give lip service to wealth management to get the assets or sell products. Offering a completely holistic and robust wealth management offering is one of the best ways to provide value for clients and build a sustainable wealth management practice. Many firms cite a fear of losing clients for all services due to poor performance as a wealth manager. This could be true if all you do is manage their assets. But for firms providing the comprehensive, holistic solution, the focus is frequently on the value of all of the services that you provide, and not centered on investments and performance.

Early in the CPA PFP world, many CPAs became investment advisors and began to manage money or work with a third-party asset management firm. While this worked for some very large firms and a select few of the smaller firms with very loyal clients, the greatest enterprise value is generally built by those offering services that are more robust, detailed and responsive when compared to other service providers from Wall Street or the insurance industry.

Proactive and holistic service includes a thorough analysis of all parts of your clients’ financial lives. This includes the core areas of cash flow today and in the future, risk management, tax planning, investment planning, retirement planning and estate planning. It also includes your ability and desire to address specific issues that arise such as education planning, elder planning for parents of your clients, or their desires to buy or sell a business. Not only do these issues need a thorough analysis at the beginning of the PFP relationship, but they need to be reviewed and updated regularly as facts and circumstances change. The level of service needed today to set your firm apart is rising. The standard of care is rising, in part due to all of the free information that clients can garner on their own alongside low-cost investment or “robo” offerings. If your value starts and stops with investments, and your model is to merely acknowledge or give lip service to the client’s deeper needs, you run the risk of being marginalized by low-cost providers.

This last part, in my opinion, is the most beneficial distinction that you can offer your clients. Your commitment and ability to make sure that every moving part of your clients’ financial lives is in order today, and stays that way forever, is the best way to demonstrate your value distinction. Proudly deliver that service and communicate that distinction clearly and directly with your clients about how your firm will make that happen.